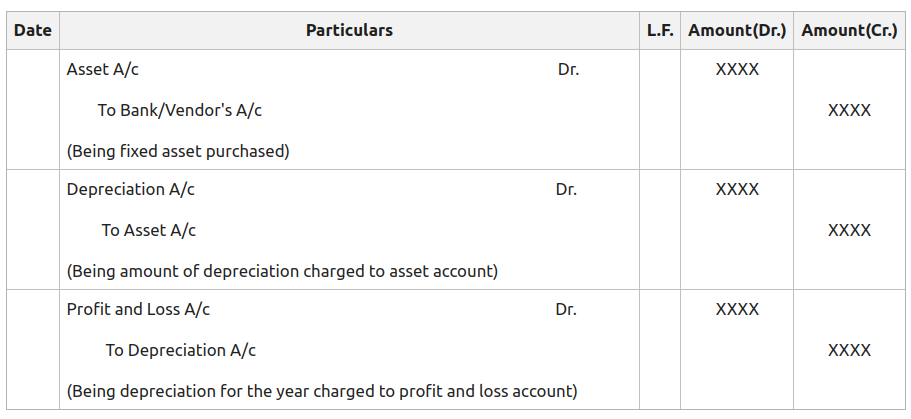

The purpose of the journal entry for depreciation is to achieve the matching principle. In each accounting period, part of the cost of certain assets (equipment, building, vehicle, etc.) will be moved from the balance sheet to depreciation expense on the income statement. The goal is to match the cost of the asset to the revenues in the accounting periods in which the asset is being used. Accumulated depreciation has a credit balance, because it aggregates the amount of depreciation expense charged against a fixed asset.

Why Does Accumulated Depreciation Have a Credit Balance on the Balance Sheet?

Any gain or loss above or below the estimated salvage value would be recorded, and there would no longer be any carrying value under the fixed asset line of the balance sheet. For example, if a company buys a vehicle for $30,000 and plans to use it for the next five years, the depreciation expense would be divided over five years at $6,000 per year. Each year, depreciation expense is debited for $6,000 and the fixed asset accumulation account is credited for $6,000. Depreciation is the gradual charging to expense of an asset’s cost over its expected useful life. The use of a depreciation method allows a company to expense the cost of an asset over time while also reducing the carrying value of the asset. Initially, most fixed assets are purchased with credit which also allows for payment over time.

FAR CPA Practice Questions: Debt Covenant Compliance Calculations

To put it simply, accumulated depreciation represents the overall amount of depreciation for a company’s assets, while depreciation expense refers to the amount that has been depreciated in a specific period. Depreciation is an accounting entry that reflects the gradual reduction of an asset’s cost over its useful life. With the declining balance method, depreciation is recorded as a percentage of the asset’s current book value. Because the same percentage is used every year while the current book value decreases, the amount of depreciation decreases each year. Even though the total accumulated depreciation will increase, the amount of accumulated depreciation per year will decrease. Accumulated depreciation is the total amount of depreciation expense recorded for an asset on a company’s balance sheet.

Is Accumulated Depreciation an Asset or a Liability?

However, accumulated depreciation plays a key role in reporting the value of the asset on the balance sheet. A depreciation expense, on the other hand, is the portion of the cost of a fixed asset that was depreciated during a certain period, such as a year. Depreciation expense is recognized on the income statement as a non-cash expense that reduces the company’s net income or profit. For accounting purposes, the depreciation expense is debited, while the accumulated depreciation is credited.

In short, by allowing accumulated depreciation to be recorded as a credit, investors can easily determine the original cost of the fixed asset, how much has been depreciated, and the asset’s net book value. Accumulated depreciation refers to the cumulative depreciation expense recorded for an asset on a company’s balance sheet. Depreciation expense and accumulated depreciation are two important concepts in accounting that help companies accurately report the value of their assets over time.

Accumulated Depreciation and Depreciation Expense: A Complete Guide

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path. Charlene Rhinehart is a CPA , CFE, chair of an Illinois CPA Society committee, and has a degree in accounting and finance from DePaul University. For an asset that’s being depreciated over five years, the sum-of-the-years’ digits would be 15 (1+2+3+4+5). For the past 52 years, Harold Averkamp (CPA, MBA) hasworked as an accounting supervisor, manager, consultant, university instructor, and innovator in teaching accounting online.

The original cost of the asset is known as its gross cost, while the original cost of the asset less the amount of accumulated depreciation and any impairment charges is known as its net cost or carrying amount. Accumulated amortization and accumulated depletion work in the same way as accumulated depreciation; they are all contra-asset accounts. For tangible assets such as property or plant and equipment, it is referred to as depreciation. what does the credit balance in the accumulated depreciation account represent Otherwise, only presenting a net book value figure might mislead readers into believing that a business has never invested substantial amounts in fixed assets. The balance sheet would reflect the fixed asset’s original price and the total of accumulated depreciation. Tracking the depreciation expense of an asset is important for reporting purposes because it spreads the cost of the asset over the time it’s in use.

The net difference or remaining amount that has yet to be depreciated is the asset’s net book value. After three years, the company records an asset impairment charge of $200,000 against the asset. This means that the asset’s net book value is $500,000 (calculated as $1,000,000 purchase price – $200,000 impairment charge – $300,000 accumulated depreciation). Accumulated depreciation is a contra asset that reduces the book value of an asset. Assume that a company purchased a delivery vehicle for $50,000 and determined that the depreciation expense should be $9,000 for 5 years. Therefore, after three years the balance in Accumulated Depreciation will be a credit balance of $27,000 and the vehicle’s book value will be $23,000 ($50,000 minus $27,000).

Accumulated depreciation is incorporated into the calculation of an asset’s net book value. To calculate net book value, subtract the accumulated depreciation and any impairment charges from the initial purchase price of an asset. This means that the asset’s net book value is $500,000 (calculated as $1,000,000 purchase price – $200,000 impairment charge – $300,000 accumulated depreciation). Instead of expensing the entire cost of a fixed asset in the year it was purchased, the asset is depreciated. Depreciation allows a company to spread out the cost of an asset over its useful life so that revenue can be earned from the asset.

- So, depreciation expense would decline to $5,600 in the second year (14/120) x ($50,000 – $2,000).

- Accumulated depreciation allows investors and analysts to see how much of a fixed asset’s cost has been depreciated.

- The balance rolls year-over-year, while nominal accounts like depreciation expense are closed out at year end.

- The simplified version of these adjustments is that a special deferred tax asset will be put on the balance sheet to serve as a way to adjust for the difference between the income statement and the cash flow statement.

- Accumulated depreciation is initially recorded as a credit balance when depreciation expense is recorded.

This would continue each year until the amount of the deduction is less than or equal to the amount that would be obtained using the straight-line method, at which point it switches over to that method. So in this example, the declining balance method would only be advantageous for the first year. To see how the calculations work, let’s use the earlier example of the company that buys equipment for $25,000, sets the salvage value at $2,000 and the useful life at five years. It is important to note that an asset’s book value does not indicate the vehicle’s market value since depreciation is merely an allocation technique. The truck has an estimated useful life of 5 years and a residual value of $10,000.